IAL Consultants: Polyurethane Chemicals and Products in Asia Pacific (APAC) 2019

IAL Consultants has published the eighth edition of its report on the markets for polyurethane chemicals and products in Asia Pacific. This study updates and expands upon the information included in the previous study published in 2017. It contains both PU product production and raw material consumption figures, with 2018 as the base year and market forecasts provided to 2023. The data in this eight-volume report includes raw material consumption by product type, by region, by country and by major end-use industry. The Raw Materials volume contains supply and demand data for all of the major polyurethane raw material types. The Major End-Use Markets volume contains an overview of the markets for PU products and a summary of trends and drivers.

Key findings and market summary

The total production of polyurethane products in the APAC region was just over 13.4 million t in 2018. The production is expected to increase by 4.3 % annually over the next five years to reach almost 16.6 million t by 2023.

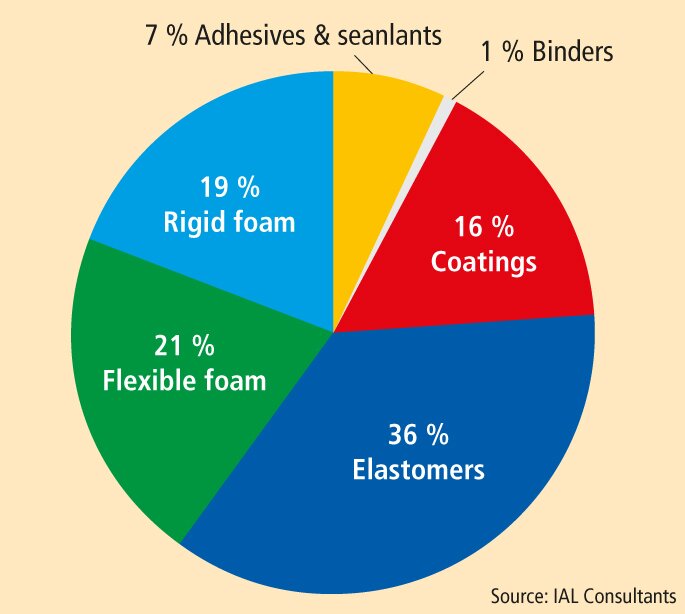

The structure of the PU industry is very different in APAC in comparison to other major global regions, with PU elastomers forming the largest product segment. This is thanks to the huge amounts of PU raw materials consumed by the synthetic leather, fibre/spandex and footwear industries. Indeed, PU elastomers accounted for some 36 % of the total APAC PU production at almost 4.9 million t. The second largest PU market segment was flexible foam at 2.8 million t, of which the vast majority was conventional polyether slabstock foam.

The geographical split of PU production in APAC is very distorted, with most production, a total of 10.4 million t, or 77.7 %, of the overall APAC PU output coming from China. There has, however, been a slight shift in the market, and unlike a few years ago, the fastest growth is now present in some South and South East Asian countries, whereas China has now moved past the stage of fast development. Nonetheless, the Chinese PU production is still expected to grow on average 4.3 % annually over the forecast period, with fastest growth coming from PU adhesive applications and flexible foam products, to reach 12.9 million pounds by 2023.

Raw materials

The APAC consumption of MDI and TDI was estimated at 3.0 million t and 1.0 million t, respectively, in 2018. The APAC MDI market is largely driven by the demand from elastomer applications and the use of PU rigid foam in appliances as well as for thermal insulation in the construction industry, whereas TDI is primarily used in flexible foam production, with mattresses, upholstery and transport seats representing the main end-use applications.

In the last few years, PU raw materials, including isocyanates, have been subject to severe price fluctuation, which has had a detrimental impact on many end-use markets, with some downstream consumers resorting to using alternative technologies and product substitution, away from polyurethanes, to meet their end needs.

|

Country |

2018 / t |

2023 / t |

2018 – 2023 / % growth p.a. |

|

East Asia |

11,843,200 |

14,446,500 |

4.1 |

|

South East Asia & Oceania |

957,300 |

1,282,900 |

6.0 |

|

South Asia |

629,400 |

883,500 |

7.0 |

|

Total EMEA |

13,429,900 |

16,612,900 |

4.3 |

|

Total APAC production of all PU products and growth rates by region, 2018 – 2023 (Source: IAL Consultants) |

|||

Flexible foam

Total production of flexible polyurethane foam in 2018 in the APAC region was estimated to have been just over 2.8 million t, of which the majority, 1.9 million t, was slabstock foam, primarily conventional polyether slabstock. Again, the Chinese production dwarfed the rest of the region. China is a huge production hub for many end-use markets for flexible foam, including furniture, bedding, footwear and automotive OEM. The growth of polyether slabstock production in China has slowed down from its peak, but remained strong in the last couple of years, mainly driven by bedding applications, whereas the high raw material costs affected furniture production. The demand from bedding has remained buoyant thanks to changing sleeping habits and a rapid increase from export markets. In addition, there has been growing demand for PU slabstock from applications such as footwear thanks to the growth in athletic footwear production, as well as packaging, garments and filter applications.

The production in South East Asia and South Asia has grown quickly in recent years in terms of volume and market share; this is due to the ongoing shift of production of furniture, bedding and footwear to this region, increased political stability, rapid growth of the economies, and rising domestic consumption in many countries, but the total output is still small in comparison to East Asia, and China in particular. The demand for moulded PU foam is closely linked to the performance of the automotive industry; this was quite buoyant in 2017, but the performance of the sector was more varied in 2018. Total vehicle output increased considerably in countries such as Indonesia, Malaysia, Pakistan and Thailand, but contracted in China, Taiwan and South Korea. Asia Pacific accounts for over 50 % of global vehicle production. Around 85 % of the passenger car production in Asia-Pacific is concentrated in East Asia, mainly in China, Japan and South Korea. The average consumption of seating foam per car has increased in line with the fall in production of small or mini cars over the last few years, and the growing popularity of larger vehicles including SUVs and CUVs.

Moulded PU flexible foam is also used in furniture applications, with most production taking place in China, but the fastest growth is taking place in South East Asia, in countries such as Vietnam and Indonesia.

Rigid foam

Production of PU products in 2018 in Asia Pacific (in t); Total: 13,429,900 t

The total APAC production of rigid polyurethane foam was almost 2.6 million t in 2018, of which almost half was destined for appliance production, above all domestic refrigeration. China is the largest producer, although the demand for PU in appliance applications has slowed down since 2015 as a result of the appreciation of the CNY, anti-dumping and trade issues as well as declining overseas demand. Prior to this, the sector was experiencing high growth rates. Simultaneously, the production of refrigeration appliances is accelerating in South and South East Asia, thanks to the growing housing market, increased urbanisation and as well as the rise in income levels. Many East Asian appliance producers have also set up production facilities in South East Asia, or completely shifted their production there.

The demand for PU rigid foam for thermal insulation in construction applications is increasing. Large numbers of buildings are poorly insulated in Asia, especially in the developing markets in South East Asia, China and South Asia, representing a large growth potential for thermal insulation materials for buildings in the region. Continuous rigid-faced panels are the largest product group for PU used in construction applications, accounting for roughly 10 % of the total Asian PU rigid foam production. PU faces fierce competition from other materials in the Asian thermal insulation market, in particular rock/stone wool when fire resistance is an important consideration, and EPS and XPS in the more price-driven markets.

Elastomers

The total APAC PU elastomer production was almost 4.9 million t in 2018 and the output is expected to increase at 4.2 % annually to reach close to 6 million t by 2023. Synthetic leather manufactured in China is by far the largest product segment. The sector was experiencing rapid growth leading up to 2014, accelerated by the growth in footwear and furniture output, the largest end-use markets for synthetic leather, but since then the growth of these sectors has slowed down due to rising wages and the resulting shift of production to other countries, as well as tightening environmental regulations, which has resulted in the closure of many small factories, and consolidation amongst the rest. The sector is growing more strongly in some other countries in Asia, including Vietnam and India, but the volumes produced remain small in comparison to China.

The second largest PU elastomer product segment in Asia is fibres/spandex, accounting for some 17 % of the total elastomer output. The sector is expected to continue to grow strongly over the forecast period, with annual growth rates in excess of 8 %, driven by increasing domestic and overseas demand, upgrades to technology and equipment, phasing out of small capacity and expansion of large manufacturers. In particular, the demand for technical fabrics grew strongly. Most production takes place in China, but significant quantities are also produced in South Korea and Vietnam.

Coatings

Total APAC production of polyurethane coatings was nearly 2.2 million t in 2018, with wood and furniture coatings representing the largest product segment at almost 40 % of the total output. Most PU coatings production takes place in East Asia, and China in particular, where the industry has settled into a period of more moderate growth. Stringent environmental inspections forced the closure or relocation of some manufacturers, and others were able to capitalise on this by expanding their capacities. In comparison to East Asia, the production of polyurethane coatings in South and South East Asia is much lower, owing to the popularity of more traditional paints such as those based on alkyd, nitrocellulose, acrylic or epoxy resins, which are much preferred in architectural and industrial applications. The lack of raw material availability has also limited the production of PU coatings.

Adhesives and sealants

The total APAC production of PU adhesives and sealants was around 890,500 t in 2018. The sector is expected to grow on average 5.7 % annually over the forecast period, driven by the increasing demand from a range of industrial sectors, particularly in the flexible packaging, footwear, construction, and automotive sectors. Most PU adhesives and sealants are manufactured in East Asia, mainly China and Japan. This is thanks to the well-established production infrastructure, mature technology and the presence of large end-use markets such as footwear, flexible packaging, construction and automotive. China is the world’s largest footwear producer and Japan is the second largest flexible packaging producer after the USA. There is only limited PU adhesive and sealant production taking place in South East Asia and South Asia. The local industry and technology are underdeveloped, and these markets are largely served by exports from East Asia, Europe and the USA.

Binders

Binders represent a comparatively small segment of the overall PU market, with the total APAC output at just 95,000 t in 2018. These products have a narrow range of applications, as well as facing competition from less expensive furan and formaldehyde binders. The main application areas for polyurethane binders are in forest products such as plywood, particle board, MDF, OSB and agri-fibre panels, with other areas of importance being in rubber crumb and foundry core applications.

|

The report “Polyurethane Chemicals and Products in APAC – 2019 – 8th Edition” is presented in the following eight volumes: Raw Materials, Flexible Foam, Rigid Foam, Coatings, Adhesives and Sealants, Elastomers, Binders, End-Use Markets. Prices start at EUR 1,100 for single volumes. The complete report is priced at EUR 14,900. Contact: |

Like this article? Share Now!

More news from this section

CPI: Finalists for 2019 Polyurethane Innovation Award announced

The Center for the Polyurethanes Industry (CPI) announced Riddell SpeedFlex Precision Diamond Football Helmet Liner and Dow Aquachill Cool Coating for Comfier Bedding as the finalists for the 2019 Polyurethane Innovation Award.

read moreSmithers Rapra: The Future of Silicone Elastomers to 2024

Global consumption of silicone elastomers will approach 500,000 tonnes in 2019 for the first time, according to exclusive provisional data from the forthcoming Smithers Rapra report, the Future of Silicone Elastomers to 2024.

read more

Write a comment on this article now